Kynda Curtis, Professor, Department of Applied Economics, Utah State University

The food system in the United States is a complex grid of farms, processors, shippers, packers, millers, and final retail grocery and food service outlets, such as restaurants, schools, hotels, and hospitals. Most food products are heavily processed; only products such as fresh produce, eggs, and milk are packed and shipped with little or no processing. Due to the large degree of food processing required, farmers receive only $.11 cents on average of every dollar we spend on food. While food production does take place in all US states, most of our food is produced in California and the mid-west. Transporting food nationwide requires complex trucking, rail, and air shipping systems. Additionally, we import and export food world-wide; in 2018 US food exports exceeded imports by about $11 billion.

COVID-19 has impacted our lives a great deal, but it has especially impacted where and how we eat. Our food system has had to bend a great deal due to both supply and demand shocks resulting from COVID-19. It has been said that while our food system is very efficient, it’s not very flexible. Here are a few questions you may have about the impacts of COVID-19 on our food system.

Why did we experience food shortages at the grocery store?

Food distribution in the US employs “just-in-time” systems, where grocery retailers track customer behavior over time and only order what they need. This means there isn’t any extra inventory, and thus when consumers began to stay home in mid-March, the spike in retail grocery purchases shocked the system and created shortages. These short-term shortages were ironed out in the longer-term as grocery store shelves today look “normal,” with few, if any, out-of-stock items.

The increased spending at the grocery store resulted from stay-at-home mandates and school closures. Americans were no longer eating at school or work, nor meeting colleagues and customers for lunch or celebrating family events with special restaurant dinners. Many restaurants were closed or only providing limited curbside pick-up meal services. Additionally, food shortages led to increased grocery store pricing. Grocery pricing nationwide increased by 4.6% from July 2019 to July 2020 (USDA ERS, 2020).

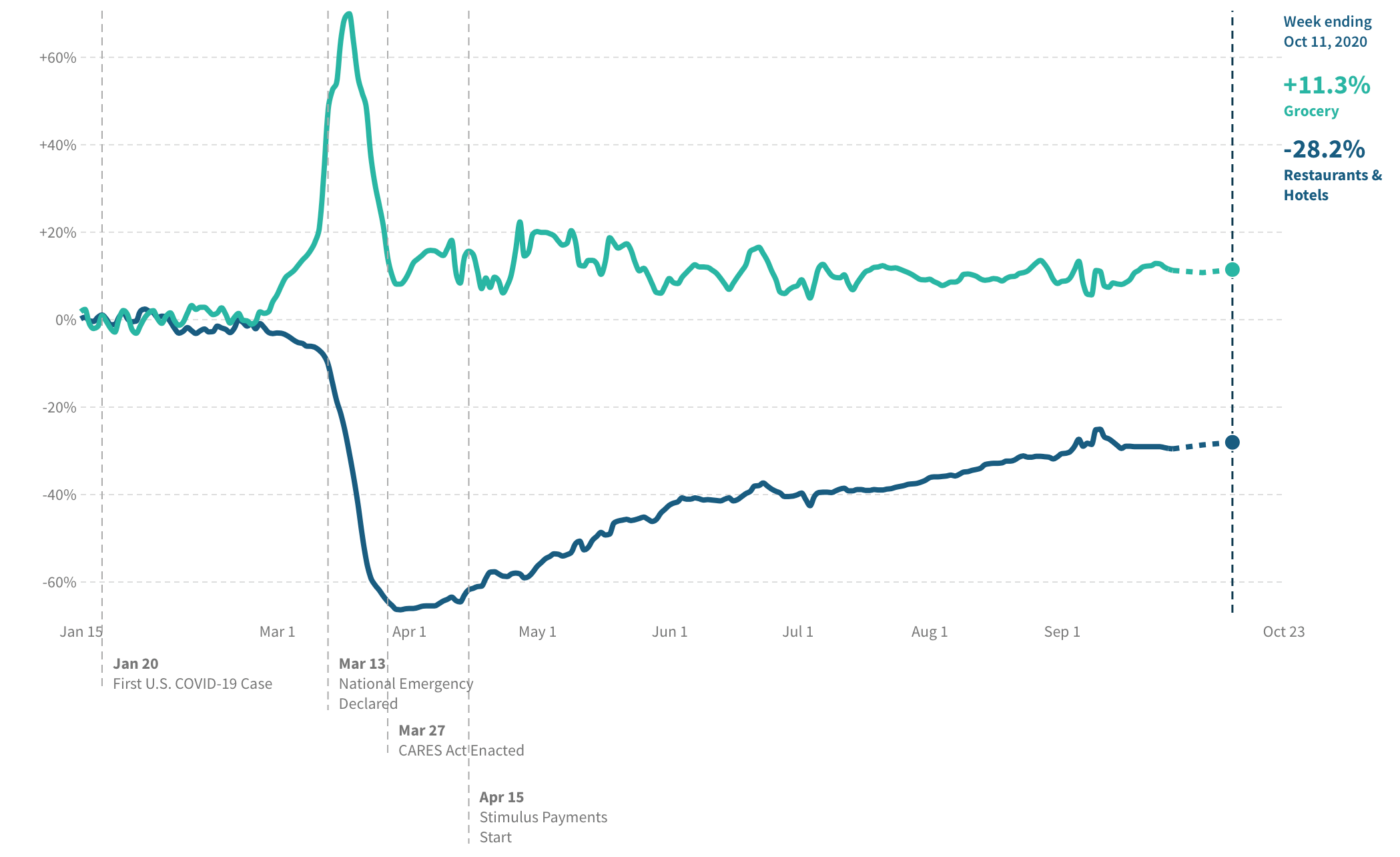

Nationwide grocery spending is still up 11.3% (as of October 11) over January 2020 levels, but down from its high of 73.7% on March 18 (Figure 1). Restaurant and hotel spending remain lower than January 2020 levels (-28.2% as of October 11), but has improved since its low of -66.7% on March 31.

Figure 1. US Grocery and Restaurant/Hotel Spending as a Percentage of January 2020 Levels

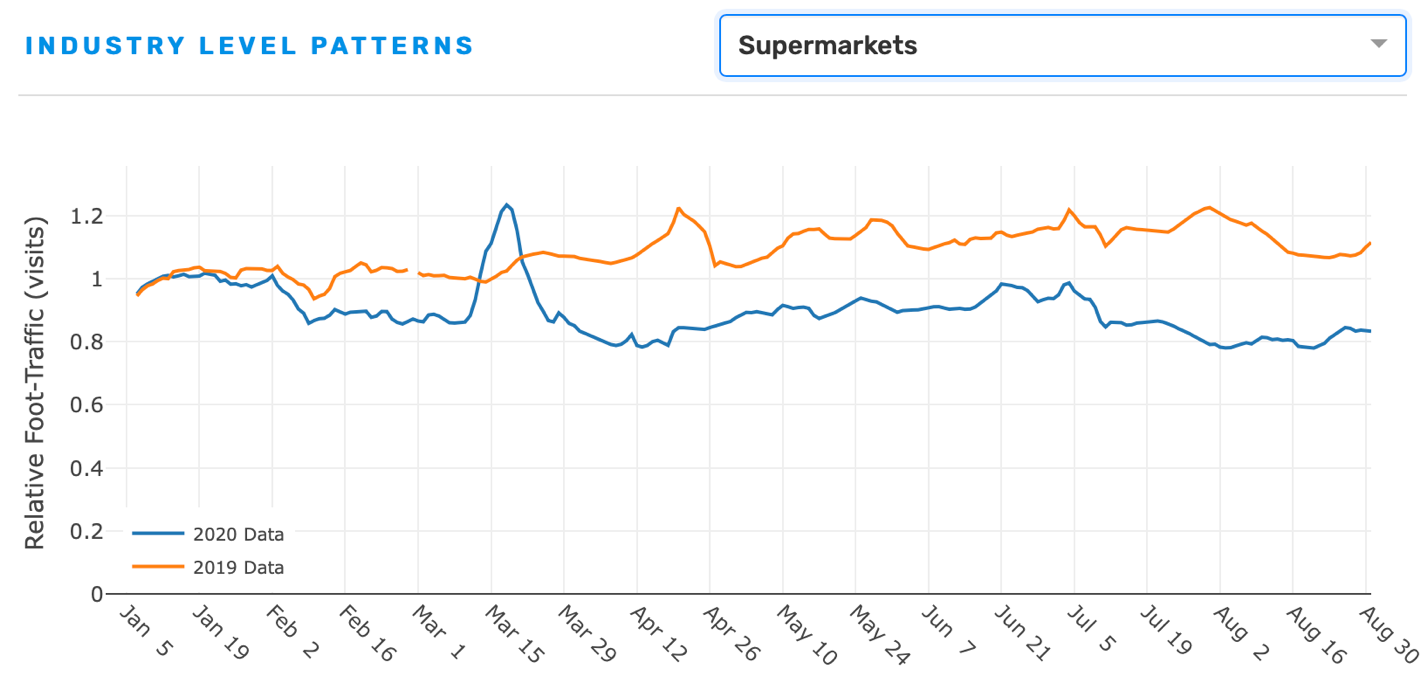

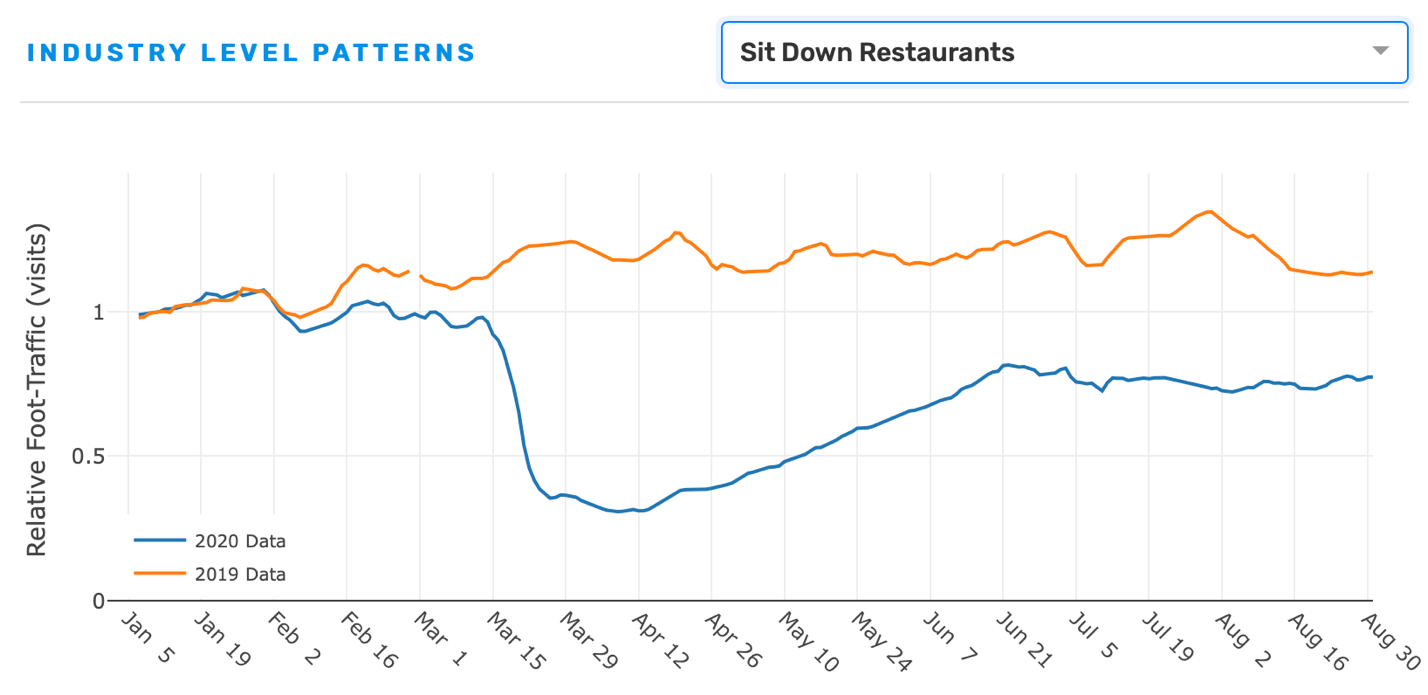

As shown in Figure 2 and Figure 3, supermarket foot traffic is 28% below 2019 levels (as of August 31) and has dropped off from mid-March highs. Foot traffic at sit-down restaurants has rebounded substantially over early April lows, but is still about 36% (as of August 31) under 2019 levels.

Figure 2. Relative Foot Traffic (Visits) for Supermarkets, 2020 vs 2019, US.

Figure 3. Relative Foot Traffic (Visits) for Sit-Down Restaurants, 2020 vs 2019, US.

Why couldn’t food bound for restaurants, hotels, and schools be rerouted to grocery outlets and food banks?

One of the primary reasons that food can’t be rerouted easily is that restaurants, hotels, schools, and retail grocery have completely different supply chains and the connections and relationships in one supply chain don’t transfer automatically to another. Also, the form and type of products used by each final market are different. For example, eggs destined for schools are often powdered, those headed for restaurants come in large packets of 36 or more, and those in grocery stores come in one dozen cartons. Milk headed to schools comes in small containers (8 oz.) and often include a chocolate option, the milk you buy in the grocery store is packaged in larger pint, half gallon and full gallon containers. Also, the variety or type of food product demanded by each final market may also differ greatly. For example, the average grocery shopper only purchases about 50 popular fruits and vegetables, but restaurants use up to 3000 different produce items.

Why were farmers and ranchers dumping milk and destroying livestock when there were food shortages?

When the demand for food dropped off heavily in the food service and school markets, products were held in storage at the processing facilities, with the packaging points of the food supply chain at capacity. There was essentially no space to put new milk and other products arriving from farms and since milk, for example, is highly perishable, it had to be dumped on farm or at delivery.

Also, due to processer closures amidst COVID-19 outbreaks at those facilities, meat processing volumes especially, declined sharply from 2019 levels (up to 40%) in late April 2020. Workers at many facilities were quarantined and others walked out demanding safer working conditions and PPE. As of July, cattle and hog processing levels were back to 2019 levels. Chicken processing levels were relatively unaffected. Meat processing is highly concentrated, as 10 plants slaughter 63% of all cattle and 15 plants slaughter 59% of all hogs in the US. Hence, the closing of just three or four plants can cause major disruptions in the meat supply chain. Genetic breeding of animals and feed lot practices create a situation where animals have to be slaughtered at a specific time in order to properly fit slaughter machinery. Also, animals can become too big for their bone and/or muscle structure if they are not slaughtered at the appropriate time, thus many animals were disposed of prior to processing.

What might increase flexibility in our food system moving forward?

The events surrounding COVID-19 have increased our awareness of the vital role that local food systems can play in providing food security when national food systems break down or are impeded. Local food systems, often referred to as short supply chains, are flexible and can more easily pivot to serve new markets. While local food demand is strong, it primarily functions with chefs and consumers, who purchase directly from growers at farmers’ markets, farm stands, and through community supported agriculture (CSA) programs or grower websites. Many aspects of a strong local food system are missing, such as millers, processors, bakers, butchers, etc. Local, state, and federal policies which better enable the success and sustainability of local food systems are needed. Consumers concerned with empty grocery shelves have turned to local food providers across the country, buying produce and meat directly from producers, who have seen large increases in CSA program participation and online sales of their products, as much as 500% in some cases. Will this trend in local food buying continue? Good question. It’s likely that many consumers who had not participated in a CSA or purchased beef from a local rancher prior to the pandemic, will continue to do so even after COVID-19, as they discover the value of the buy local experience (freshness, taste, community, etc.). But others, will return to their pre-COVID purchasing patterns.

Accessibility

If you need assistance accessing any content on this webpage, please contact Kynda Curtis, kynda.curtis@usu.edu.